Costing Materials using First in First Out (FIFO) Method Periodic.

From the word itself, the first items that will come in (or purchased) , will be the first item that will be issued (or used) when there would be an issuance of materials.

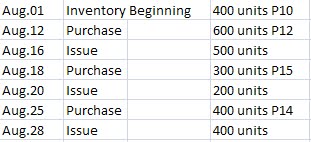

CONSIDER THE FOLLOWING SITUATION:

Using the periodic method, we are going to compute for the total units at the end of the month by deducting the total units purchased and total units issued:

Total units purchased of 1700 is computed by adding the beginning inventory and all the purchases:

400 units+600 units+300 units+400 units

Total Units Issued is computed by adding all the issued units:

500 units+200 units+400units

Second, we will compute for the ending inventory:

Now this would be the bloody part of the explanation. :))

Okay. As mentioned earlier,the first items that came in (or were purchased) will be first to be issued (or used). Please bear with my explanation. :))

Please refer to the given situation.

On Aug.01, you have 400units@P10, and on Aug.12, purchases of 600units@P12.

On Aug16, you issued 500 units.

So from the concept of FIFO Method, to issue that 500units, you will use first the 400units(Aug.01)@P10. Your beginning inventory then of 400units will be used up. So to issue the remaining 100units (to complete the 500 units that has to be issued), we are going get that from the 600units@P12(Aug.12). Now you have a remaining 500 units@P12(Aug.12).

On Aug.18, you purchased 300units@15.

And then, on Aug.20, you issued 200units. To issue this,you must get it from the 500units@P12(Aug.12). And so, you have now 300units@P12(500u-200u)remaining, and another 300units@P15(Aug.18).

On Aug.25,you purchased 400units@P14. So now you have 300 units@12(Aug.12),300units@P15 (Aug.18) and 400units@P14(Aug.25).

On Aug.28,you issued 400units. To issue this, you will use the 300 units@P12(Aug.12) first. And then the remaining 100 units@P15(to complete the 400 units that has to be issued) will be issued using the 300units@15(Aug.18).

Now,you have a remaining 200 units@P15(300u-100u)(Aug.18) and 400units@P14(Aug.25) on hand.

I hope I made you understand that. :)) Maybe if you will refer to the perpetual table below, you will get what I'm talking about. :))

COMPUTING FOR THE ENDING INVENTORY

Remember we first computed the total units at the end of the month which is 600 units?

To compute for the ending inventory:

We will use first the 200 units at P15(Aug.18), then 400 units at P14 (Aug.25) And that would be:

And then we compute for the cost of materials issued/ used:

Total purchases is computed as 600 units+300 units+400 units

And there you have it, FIFO Method Periodic!!!!

Yey!!

Did I help you somehow??? ♥